Victor Davis Hanson writes about what happened at Stanford.

Tax me harder

Rather than reconsider the usefulness of skyrocketing borrowing for Covid stimulus, overpriced pipelines, battery plant subsidies and a war in the Ukraine, among many other programs, the federal government seems intent on making sure that productive individuals pay far more tax than they already do.

If these measures don’t trigger a recession, nothing will.

If enacted, this could bring the top combined marginal tax rate, once provincial tax is factored in, to approximately 56 per cent in British Columbia, Ontario, Quebec and Nova Scotia, and to 57 per cent in Newfoundland and Labrador.

No Sense Anywhere

Neil Oliver talks about the war against people.

House of Cards

When even the leftist corporate media starts to pick up on the perilous state of the banking system, you know things are going to get a lot worse. This is what zero percent interest rates get you combined with government sanctioned accounting tricks that let you invent whatever asset valuations suit you.

In other words, if banks were suddenly forced to liquidate their bond and loan portfolios, the losses would erase between 77 percent and 91 percent of their combined capital cushion. It follows that large numbers of banks are terrifyingly fragile.

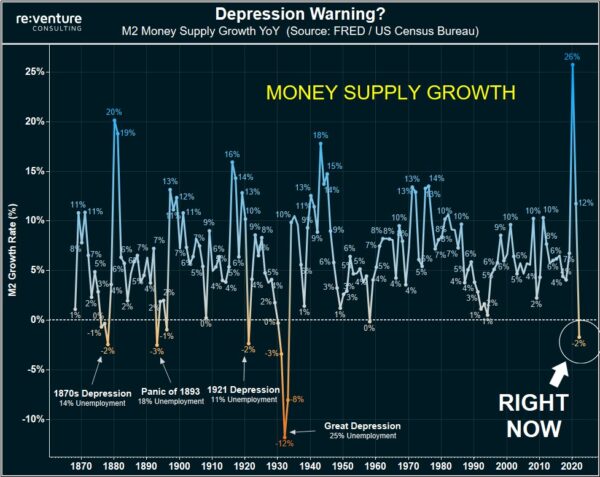

Left Coast economics

Who needs surpluses when you’ve got votes to buy? You would think with the recent crappy news coming out of financial markets, any government with an actual budgetary surplus would at least consider paying down some debt, but not in BC anyway. In any event, it would be helpful if the government at least knew where the money was going.

In a recent column, CHEK News legislative correspondent Rob Shaw wrote that the B.C. Legislature was approving spending items so quickly that MLAs often couldn’t explain where the money was going or why it was needed.

Shaw wrote when Agriculture Minister Pam Alexis was queried on why she had requested an extra $111 million in spending, she replied by reading her own press release.

Biden’s America

Victor Davis Hanson explains that we are the new Byzantines.

Counterfeit Credit

Economist Keith Weiner goes into the history behind the implosion of Silicon Valley Bank and why it’s premature for Keynesians to declare victory. As we write this, there seems to be trouble brewing at Credit Suisse. The fact that one of the world’s largest banks is on the ropes should give pause to Canadians who are dismissive of any possibility of a bank run just because Canadian banks are so massive.

The root cause of the collapse of SVB was not stupidity at the bank, insufficient regulation, or corruption at the ratings agencies. The root cause is government interference in money and credit, especially including its irredeemable currency which necessarily inflicts interest rate instability upon the world.

During periods when interest rates are falling, most people love it. Who would dislike endless bull markets and hence capital gains, and rising transaction volumes, and hence profits for investment banks? Economists praise it as a “strong economy.”

The economy was not strong. It was in a false boom, during the Fed’s binge phase. When the Fed went into purge mode, the boom turns to bust (this is starting to happen, but not fully realized yet). In the bust, banks fail, depositors lose their cash, etc. And the pressure grows to bail everyone out, thus leaping back into binge mode and another boom phase.

Things That Make You Go Hmm…

One bank bailout leads to another.

Funny Money

Armstrong Economics- The Banking Crisis is Global – Not Confined to the USA

This is a warning to all small banks. Understand the REAL trend or you will NOT survive. Major capital is fleeing the long-term and rising into the short-term because they see rates are rising and any long-term bond investment during a period of war is going to be a major losing trade. Do not get trapped by the yield curve and understand that this trend is in play into 2025.

Armstrong Economics- The Unfolding Bank Crisis

I will offer this recommendation (publicly) for my ear is turning red from all the phone calls. As for the Biden Administration, if they DO NOT heed my warning, our forecast will be devastating. The Biden Administration MUST stand behind ALL deposits – not the $250,000 FDIC limit. If they do not, small businesses will pul; excess cash from banks, switch to 30-day T-Bills at a brokerage house, and say screw the FDIC and the Biden Administration’s anti-rich (small business which employs 70% of the workforce).

Canada is in the best of hands…

*Update: More than 30 banks have been placed under trading halts.

Do as I say, even if it kills you…

Without a doubt, the collapse of Silicon Valley Bank will be a cue for every Keynesian on earth to pound the table and call for more regulation, as if too much freedom is what causes businesses to go bust. As economist Daniel Lacalle points out, SVB did exactly what banks had been told to do post 2008. Its collapse was the result.

SVB was the poster boy of banking management by the book. They followed a conservative policy of adding the safest assets -long-dated Treasury bills- as deposits soared.

SVB did exactly what those that blamed the 2008 crisis on “de-regulation” recommended. SVB was a boring and conservative bank that invested the rising deposits in sovereign bonds and mortgage-backed securities and believed that inflation was transitory as everyone except us, the crazy minority, repeated.

SVB did nothing but follow regulation and monetary policy incentives and Keynesian economists’ recommendations point by point. SVB was the epitome of mainstream economic thinking. And mainstream killed the tech star.

Juxtapose!

The Telegraph- Ukrainian healthcare is better than the NHS

If you have read and struggled to believe stories about Ukrainians living in the UK returning to their native country for medical treatment, let me tell you that I am one of them. Having given up on the NHS, I flew to Poland and crossed the border. Later that day, amid air raid sirens, I visited a hospital. By the evening, I had the relevant medicines to get me back on the mend.

Collateral damage

Deposit insurance in the U.S. covers a depositor up to $250,000, but if you’re a medium size business or larger, there’s a good chance you have a lot more cash than that tied up in a bank at any given time. What happens when there’s a bank run and most of your company’s operating cash gets trapped in a receivership proceeding? We’ll find out soon enough. This is clearly another Bear Stearns moment.

…the Bank announced a loss of approximately $1.8 billion from a sale of investments and was conducting a capital raise (which we now know failed), and despite the bank being in sound financial condition prior to March 9, 2023, “investors and depositors reacted by initiating withdrawals of $42 billion in deposits from the Bank on March 9, 2023, causing a run on the Bank.“

As a result of this furious drain, as of the close of business on Thursday, March 9, “the bank had a negative cash balance of approximately $958 million.”

Scroll down the article to see the list of companies with deposits at SVB: Roku, Roblox and Rocketlab USA to name a few.

Just a little poke!

Along the lines of what Dr. John Campbell has been saying regarding the importance of aspiration when administering vaccines, medical researcher Marc Girardot has developed a hypothesis about what might happen when the vaccine is injected into a vein instead of a muscle. His hypothesis goes a long way to explaining the variety of reactions to the vaccine ranging from none at all to sudden death.

The article is well worth the read and comes with a lot of visual aids.

In some instances, the needle might hit a small vessel and only inject a fraction of the standard doses. In other cases, a large portion, if not the entire dose, might be injected, leading to a much greater transfection potential of the endothelial linings of the blood vessels.

When the immune hit is one single cell, a neighbouring cell will duplicate to replace the missing cell, and the endothelial wall will repair perfectly. When multiple cells are hit simultaneously in a concentrated fashion, the natural process of repair no longer works.

The Censorship Industrial Complex

Matt Taibbi's opening statement on the Twitter Files and the censorship industrial complex:

"Twitter, Facebook, Google, and other companies developed a formal system for taking in moderation requests from every corner of government, from the FBI, DHS, HHS, DOD, the Global… pic.twitter.com/BbMoSYNiR2

— KanekoaTheGreat (@KanekoaTheGreat) March 9, 2023

It’s Probably Nothing

Biden’s America

Victor Davis Hanson on how criminality has become a lifestyle choice.

Indecipherable wokeness

If the city of Winnipeg goes ahead with the proposal to rename Bishop Grandin Boulevard, one can just imagine what a future 911 call might sound like:

“911. What is your emergency?”

“I need an ambulance on the corner of St. Mary’s and Bishop Grandin. We have….”

“I’m sorry sir, but St. Mary’s and what street?”

“Oh, um,… Abino,…, Abinjoey, Mika…ugh, you know, the street that used to be called Bishop Grandin….”

“I need to remind you sir that street is no longer called by its hurtful colonial name. Do you mean Abinojii Mikanah Boulevard?”

“Sure. That sounds about right.”

Zero percent payback time!

Remember when consumers enthusiastically went on a spending spree in the early stages of the pandemic, helped along by zero percent interest and a bunch of stimulus cheques? It appears that their enthusiasm is waning now that the bills are coming due.

At the height of the Covid-19 pandemic, with his job as a delivery driver bringing plenty of overtime and the cost to borrow at record lows, James Kebe went on a spending spree. He leased a boat and an all-terrain vehicle, and when his bank offered him a bigger line of credit, he maxed it out.

Then interest rates started rising at their fastest pace in generations. And because Kebe’s line of credit had a floating rate, his monthly payments soared, too. The cost of his debt has now outpaced his take-home pay by C$900 ($660) a month, leaving him with little choice but to enter a form of creditor protection that will see his toys repossessed…

O, Sweet Saint Of San Andreas

The power of prayer.

Let Them Eat Taser