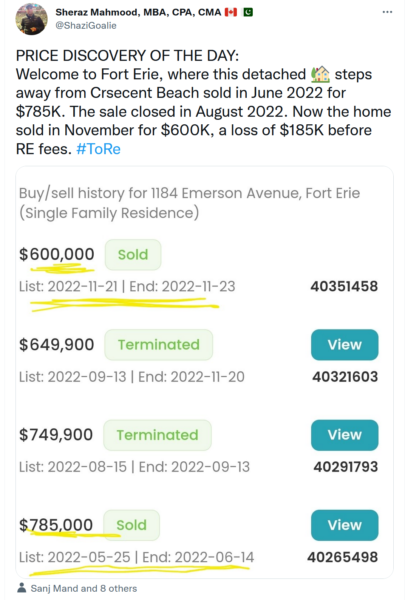

For anyone who thinks that our Canadian recession is going to be mild or a “soft landing”, they might want to consider what impact a $185,000 loss on a house sale is going to have on the personal finances of a growing number of people.

For anyone who thinks that our Canadian recession is going to be mild or a “soft landing”, they might want to consider what impact a $185,000 loss on a house sale is going to have on the personal finances of a growing number of people.

You can have the same monthly payment on the same house at 8% interest as at 1% interest.

You just have to change the purchase price a little. Maybe halve it or so.

Pop! Goes the bubble.

Variable rate mortgages like Canada’s make this much worse, as existing mortgages get repriced, and the principal does not.

Depends.

If it’s your personal residence, it’s all relative, as the “new” address should also be reduced a similar amount, if you are doing your homework.

If it’s a rental, take a bath.

The biggest impact may be with new construction. Wages, materials and taxes aren’t being reduced, so, either they sell at a reduced price, and the developer (and unpaid contractors) take a bath, or it diesn’5 sell, with the same outcome.

Don’t worry, Emperor for Life Justin will give all such sad-looking home owners an anti-inflation cheque to cover the difference and everything will be alright again. The Canadian media will marvel at his ability to solve two problems with a single simple solution.

Just like Sid Viscous’ friend Nancy was alright again after being filled up with heron in this little commemorative shimmy from Nina Hagen…

https://m.youtube.com/watch?v=mcmDxgj5BIc

Justin will get a pay raise on April 1, 2023.

Possibly another $21,000

That would give him a salary of $400,000/year.

And he may think it’s time to purchase new boats for Harrington Lake. The previous 8 boats he charged to tax payers are getting a little old.

Joe: yes, as we all know the only way to beat inflation is to pump billions of borrowed dollars into the economy, including government pay raises. Same for deflation. The answer to all problems is more dollars. It makes the dollar more valuable. Like Alfred E Newman said “I don’t spend too much time worrying about monetary policy…”

Maybe it’s just me, but I have a bit of a problem with the narrative.

When my girlfriend and I bought our house in ’01 it was a place to make a home first.

It was also a place to live together.

An investment yes, but a very, very distant third.

Has it appreciated? Well duh? Has the value gone down a pantload from 12-18 months ago?

We don’t fckn care.

We still need to live somewhere.

If you’re a speculator, each shit.

If you bought a house as an investment first and a home second or third and now you’ve got to sell, tough shit.

If you bought a home first and things went sideways and you suddenly have to sell and you’re going to take it up the hoop, you have some of my sympathy, but not all of it. Shit happens. To everybody.

Stay a renter or don’t buy something way beyond your means.

And anyone who didn’t see rising interest rates coming is too stupid to be a home owner.

They might be as dumb as people who want a static climate.

If you’re a speculator, each shit.

If you bought a house as an investment first and a home second or third and now you’ve got to sell, tough shit.

Exactly. If you bought in August to flip in November, you are the problem. Eat each and every shit.

Houses should be homes.

100% correct. They are fn flippers.

Buddy

And still, rates have not gone ballistic.

I recall quite clearly the early 80’s

21%….

Bluddy

You a 12 year old school girl or what?

I buy to flip at times, but know when not to!

Now go eat schitt!

The “cures” that they are contemplating to avoid scenarios such as this include:

– interest only mortgages

– 40 year mortgages

– expanding CMHC to…. something

welcome to perpetual real estate slavery.

“We’re from the gubmint and we’re here to “help””

They bought in June and sold in November… They are just flippers trying to make buck. boohoo.

I don’t have a problem with flippers, as long as they’re actually trying to improve the homes they buy (and Lord knows, a lot of homes could use some serious remediation before being put on the market; damn near everything in the Lower Mainland comes to mind…).

Yeah. $5000/month for a crappy one-bedroom in Vancouver isn’t enough. Better renovate, flip and up the rent.

Vancouver, where $50 000 a year income gets you a place in the tent city of the lower east side.

Except there are plenty of places to live in the Lower Mainland without being in Vancouver itself.

Problem is, mass immigration has put too much pressure on housing along with microscopic interest rates.

That said, we are early in the correction phase. There’s a lot of air yet to be popped out of the Real Estate balloon

Or maybe somebody lost their job because they wouldn’t get “vaxxed”.

As far as I’m concerned … this should be the fate of every house-flipper who applies some cosmetic crapola … and tries to make money for nothing.

3 obvious things:

1) The pricing information does provide sufficient information to why

2) There will be a whole lot of appraisers that are going to be run out of business because they are doing a shit job of appraising houses

3) a goodly portion of the losses will be socialized, because the people who cannot make the down payment at 20% and get the CHMC supported mortgage have a whole lot less to lose than someone who paid a 20% down payment on a house that just got that 20% haircut

Also, as a side note, there is no way that it costs ~1% of the house to process a land transfer, so where is the land-transfer tax money going? (in toronto, it’s charged twice, so john tory can get paid to make a mess of the city)

Hopefully it is within the city limits of Ottawa, Toronto and Montreal. They deserve it.

It does sound like a “liberal” problem.